What is a 40-Year Mortgage?

Story Location:

49 Baltimore Avenue

Rehoboth Beach, DE 19971

United States

When you open a mortgage, your loan originator will help you choose an amortization period, or the length of time you will make payments on the loan to pay it off. And while you may think you have to choose a 15-year or 30-year mortgage term, because those are two very common options, you may want to consider a 40-year mortgage.

A 40-year mortgage is not ideal for everyone. It takes longer to build equity and you will likely pay more in interest over the life of the loan. But, depending on your circumstances, it might make sense for you. Read some of the potential benefits below and see for yourself.

Benefits of a 40-Year Mortgage

A mortgage loan amortized over 40 years may be the right choice if you:

- Want to get more bang for your buck on a more expensive home

- Want lower monthly payments

- Want to take advantage of larger cash-flow

- Aren’t planning on staying in your home forever and want a more affordable option

- Have trouble qualifying for a mortgage with higher monthly payments

Most first-time homebuyers are concerned with affordability – how much will my mortgage payment be?

1. Stretch Your Home Budget

If your house-hunting budget is centered around what your monthly mortgage payment will be, a 40-year loan could be a great way to stretch that a little bit. For example, let’s say you wanted to keep your monthly principal and interest payment (your mortgage payment before taxes, insurance, etc.) below $1,500 – but your dream home was a little over budget to make that happen. If you chose the 40-year mortgage loan, your monthly payment will be lower.

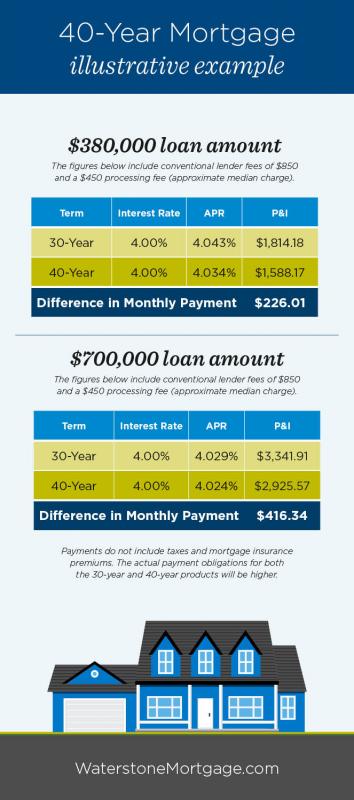

Here’s a table that looks at monthly payments to demonstrate how a 40-year mortgage might allow you to purchase more house than the 30-year option. Remember, though, that you are still likely to pay more in interest over the life of the loan with the 40-year mortgage.

2. Lower Monthly Payments

Monthly mortgage payments can often be less than rent, especially with rising rent prices and historically low interest rates

For homebuyers concerned about the cost of their monthly payments and want the lowest possible payment, a 40-year amortized mortgage loan may be a solid option.

3. Increase Your Cash-Flow

Because your monthly payments will be lower, spreading your home loan repayment period out over a longer length of time will keep more cash in your pocket each month. This is ideal for those working to pay down other expenses (auto loans, student loan debt, medical bills, etc.), but it can also be great for those who just want more freedom to use that extra money however they want to.

4. Affordable Short-Term Housing

Did you know many homebuyers – first-time homebuyers especially – choose not to stay in their home for the entire length of their mortgage? If you are purchasing a starter home, or simply don’t plan on staying in your new home forever, a 40-year mortgage could work out in your favor by allowing you to have lower payments while you live there. Forty years seems like a long time, but if you’re planning on staying in your house for just 3-5 years, you might want to save some money and choose the loan option that offers the lowest monthly payments.

5. Get Qualified More Easily

In addition, some homebuyers need a lower payment to qualify. A major part of getting a mortgage is your debt-to-income ratio (DTI), which is important to lenders. DTI is the ratio between your monthly debts and your monthly income.

If your DTI has a little less wiggle room, it’s important to keep your debts (including your housing payments) low, so choosing a mortgage option that allows for lower payments could be the way to go. Simply put, the 40-year amortized home loan could make the difference between achieving homeownership or not.

While a 40-year amortization is not ideal for everyone, folks struggling with their debt-to-income ratio may think this is a perfect solution. It takes longer to build equity with this amortization schedule, but it’s better than the equity earned while renting – none!

Homeownership strengthens families and communities, and it’s still a major part of the American dream. Ready to get started today? Find a local loan originator near you.

This article is presented to you by Waterstone Mortgage. Please click here to read the full article.